Long-Term Care Insurance and Home Care: What’s Actually Covered

Long-term care insurance is one of those things people buy and then, understandably, try not to think about. It sits in a filing cabinet. The premiums get paid. And then the moment arrives — and the family suddenly needs to understand what this policy actually covers, how to use it, and how quickly they can access the benefits.

Most families we work with have never had to navigate this process before. Here’s a clear, practical guide — without the policy jargon.

What Long-Term Care Insurance Is Designed to Cover

LTC insurance was designed specifically to cover the kinds of services that standard health insurance and Medicare do not — extended personal care, supervision, and help with daily living activities. Exactly what Agape provides.

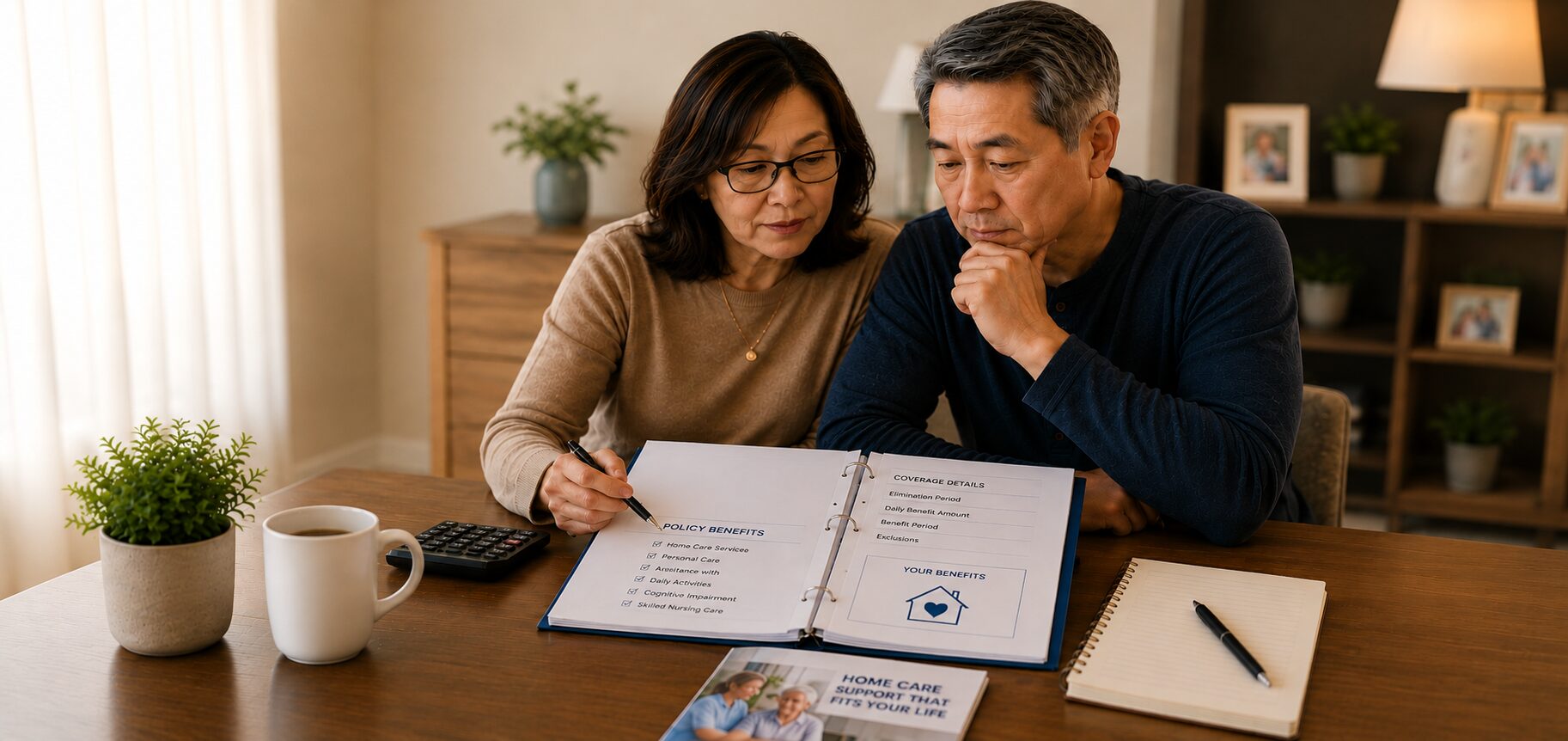

Typically Covered Services

- Personal care at home — bathing, dressing, grooming, toileting, mobility assistance, meal preparation

- Home health aide services provided by a registered aide

- Adult day services

- Assisted living and memory care facility costs

- Skilled nursing facility care

The Two Things That Trigger Benefits

1. A Benefit Trigger

ADL deficits: The policyholder needs substantial assistance with at least two Activities of Daily Living — bathing, dressing, eating, toileting, transferring, or continence.

Cognitive impairment: A diagnosis of Alzheimer’s or another form of dementia requiring substantial supervision.

Important: Your parent does not have to be completely incapacitated to qualify. Needing hands-on assistance with bathing and dressing may be sufficient — even if they can still walk and feed themselves independently.

2. An Elimination Period

The elimination period is the waiting period before benefits begin — similar to a deductible, but measured in days of qualifying care. Common periods are 30, 60, or 90 days.

Note: Some policies count calendar days; others require actual service days. This distinction can significantly affect the waiting period length. Read your policy or call the insurer directly.

What Medicare Does and Doesn’t Cover

Medicare does not cover non-medical personal care for ongoing, chronic needs. Full stop. Medicare may cover short-term skilled nursing visits following a qualifying hospital stay — but once the skilled need resolves, that coverage ends. If someone tells you Medicare will cover long-term home care, they are mistaken.

How to Start an LTC Insurance Claim — Step by Step

Step 1 — Find the policy. Locate the actual policy document. The declarations page shows the insurer, policy number, and key benefit provisions.

Step 2 — Call the insurer to initiate a claim. Ask: What documentation is needed? What is the elimination period? How are benefits paid — reimbursement or indemnity?

Step 3 — Get a physician’s statement. Most policies require written certification from a physician confirming the benefit trigger criteria are met.

Step 4 — Complete a plan of care. Some policies require a formal written document outlining care needs. We prepare these for our clients and can coordinate directly with the insurance company.

Step 5 — Begin tracking from day one. Keep detailed records of care dates and expenses. This documentation supports your reimbursement once the elimination period is satisfied.

We’re Here to Help

Agape Home Care has served hundreds of families across Orange County for over 14 years. We answer our own phone — 24 hours a day, 7 days a week.

(949) 690-9990Request Free Assessment

✓ Licensed Home Care Organization

✓ All caregivers CDSS-registered

✓ Serving all of Orange County

✓ Same-day placement available